Getting Ahead of the Affluent Millennials

Written by Lawrence Gonzalez, CFE and Financial Literacy Educator

We are living in the age of the nouveau rich, Black excellence, Sharper couture, and #TravelNoire. Every semester breeds a new batch of college grads who hope to start at $60,000 or more with a C-suite career in the city. The ultimate grown and sexy fostered by years of Sex in the City, and every sitcom known to man.

From the look of my Instagram, FB feed, and Linkedin, it would appear that we moved beyond struggle culture (Post racial and Post-Obama obviously). However, as one half of the “Rich and Regular” personal finance blog, Kiersten Saunders describes “the Financial Independence, Retire Early” movement otherwise known as FIRE community as “burning too male and too white”.

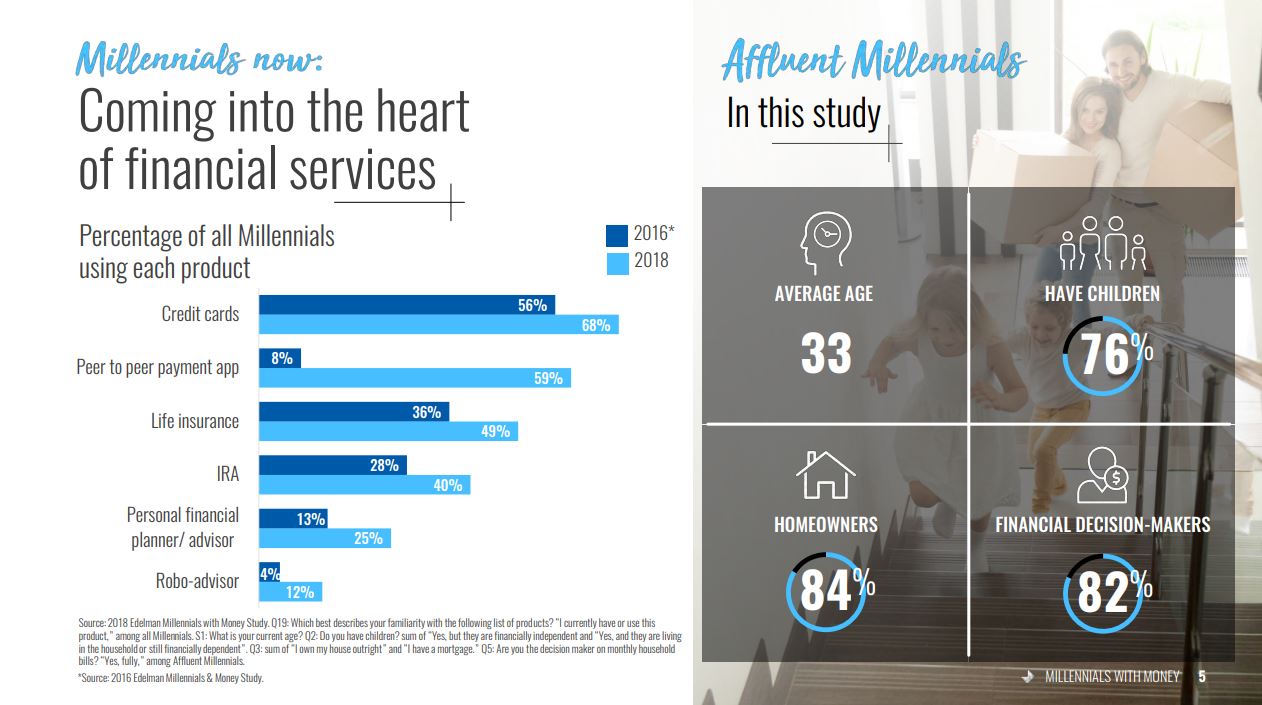

Investopedia is preparing to launch its titular millennial research that quite frankly excludes all other sectors. They are tackling the patterns of the rich and affluent set to inherit over $59 – $68 trillion dollars in the next several years. A survey which reflects the greatness and success of many living on the East and West coast. 5 minutes into the #FinCon19 session, it became obvious that millennial households making less than $100,000 per year, aren’t that important in the grand scheme. Fodder for slaughter, the non-affluent millennials otherwise known as the normal poor folks who already feel excluded from the economy, education and politics while swimming in student loan debt, credit card interest expenses, and living paycheck to stress, are in for a rollercoaster ride filled with Instagram jealousy.

In order to avoid working 50 hours for 50 weeks (out of the year) for 40 years with nothing to show for it, let’s band together and beat affluent culture. We might not have the trillions in cash infusions, but we have each other. And guess what, those rich suckers are willing to pay. They have money that’s ready to transfer to our community. Here are four things you can do today, which the financial experts call “evergreen” information:

In order to avoid working 50 hours for 50 weeks (out of the year) for 40 years with nothing to show for it, let’s band together and beat affluent culture. We might not have the trillions in cash infusions, but we have each other. And guess what, those rich suckers are willing to pay. They have money that’s ready to transfer to our community. Here are four things you can do today, which the financial experts call “evergreen” information:

-

Figure out your own priorities.

What your grandma used to say is true. We are all born to say and do something uniquely special. Find out what your own priorities are. If you love to paint, sing, dance, read books, write code, etc. Make a top ten list. Now pick out your top five. Those are your life priorities. If you like to stunt on “them” on Instagram so be it. STUNT but start cutting all utter aspects that aren’t of value to you.

For example, I hate networking and happy hours. Both combined, are torture to me. So I don’t do either. I love helping people. Reviewing resumes while drinking wine ($20 for 6 servings). I love getting croissants and coffee in the morning at least three times a week ($21). All of that saved me money because I wasn’t s

pending $15 on each drink. The more time I spend writing and reviewing, I realize I needed less TV (saved $80/month). I’m saving more than I spend on things that I love.

Try it out. You will feel the difference in a month.

Find a way you maximize your priorities and cutting out the useless parts. It saves you money, hones your skills, and makes your marketable long term. Affluent millennials know what they want. You should too.

-

Run and don’t walk to start a side hustle.

This is where you find out what sparks your mood and creativity. It will teach you discipline and setting expectations through failure. This is the real world work you need to stick it to the affluent. Think of Etsy. There are rich people willing to pay for your creativity. It’s your time to shine.

Fill your time with what you love to do and you will

find a market that’s willing to give you a shot.

-

Stay Ready

Thirdly, I can’t stress it enough, “Don’t get ready but stay ready”.

Thirdly, I can’t stress it enough, “Don’t get ready but stay ready”.

My favorite Podcasters from Paychecks and Balances were in town running a segment. Their special guest ran late. They asked me to jump on. Sometimes that’s how opportunity happens. Being around and not even hesitating especially if it cost nothing to participate. It’s akin to playing your first professional NBA game. If you are halfway decent and in good shape, just roll with it.

The same can be said for bad things happening to you. Most Millennials (affluent or not) are struggling to maintain their lifestyle. You wouldn’t have to maintain it if you never raised it up so high, to begin with. I know it’s hard to save for a rainy day while you are going through hurricane season but we have to. Sacrifice here and there, if you can’t save six months’ worth of expenses, save three. If you can’t save three, save one. Just save. Image if your favorite celebrity crush wanted to meet you in six months if you have at least one month of expenses saved. You would do whatever it takes.

I went from renting for $1,200/month plus my portion of utilities to renting for $650 per month in the DMV area. I saved at least $600 per month which I used to pay down debt, travel and ultimately to buy a home.

-

(Pay) Attention and Get started Today

Pay attention to your money. If you can’t remember where your last paycheck went or if your next paycheck is already promised to something else, you know it’s uncomfortable. Let’s make the change. It is time to put pen to paper. Use Mint.com to track and know where your problem areas are.

Check out the financial literacy tools and resources provided for free by the Consumer Financial Protection Bureau. Stop trusting the scammers. Go to verified experts.

Final Thoughts

These rich and affluent millennials are getting ready to live their best lives, let’s get ready to get rich off of them. They might be more educated but we have something they will never have. We know what it is like to be hungry. Have faith. Do it for yourself, your friends, and your family. We stand to gain way more if we support and grow together.

For even more content such as this, stay connected with my Linktr.ee/GQ_accountant. You might also like A Man’s Guide to Not Going Broke While Dating, Time to get your very own Linkedin Address, or The Seven Stages of Financial Freedom for Millennials. As always, share, like and definitely begin having the conversation about money before it is too late.

Bonus Resources from the author:

Between Mint.com and Personal Capital, I’m gonna go with Personal Capital because A. they give you $20 Amazon gift card with my referral link (once you complete it), B. It’s what the big CEO-types use. Why not? No matter how you slice it, it’s FREE to use. https://lnkd.in/dD9K_-5. Additionally, download and print out the NetMax Plan that help me go from NEGATIVE $110,000 to POSITIVE $200,000 in net worth in 5 years. We also have them for NetMax Plan – Single Parents, and for NetMax Plan – couples.